Owning a home is a dream for many. But what if your dream home could also reduce your tax burden?

That's exactly what Section 24b of the Income Tax Act offers. If you’ve taken a home loan, this provision allows you to deduct the interest paid on your house loan from your taxable income.

Whether your house is self-occupied or let out, Section 24(b) can help you save significantly every year.

Let’s understand this section in detail, its limit, conditions, applicability, & how you can benefit.

What is Section 24b of the Income Tax Act?

Section 24(b) is a part of the broader Section 24 of the Income Tax Act, which deals with income from house property.

Specifically, Section 24b permits deductions on the interest of a loan taken for:

- Purchase

- Construction

- Repair

- Renewal

- Reconstruction of a house property

This deduction is available under the head “Income from house property” & is separate from the principal repayment benefit under Section 80C.

How Much Deduction Can You Claim?

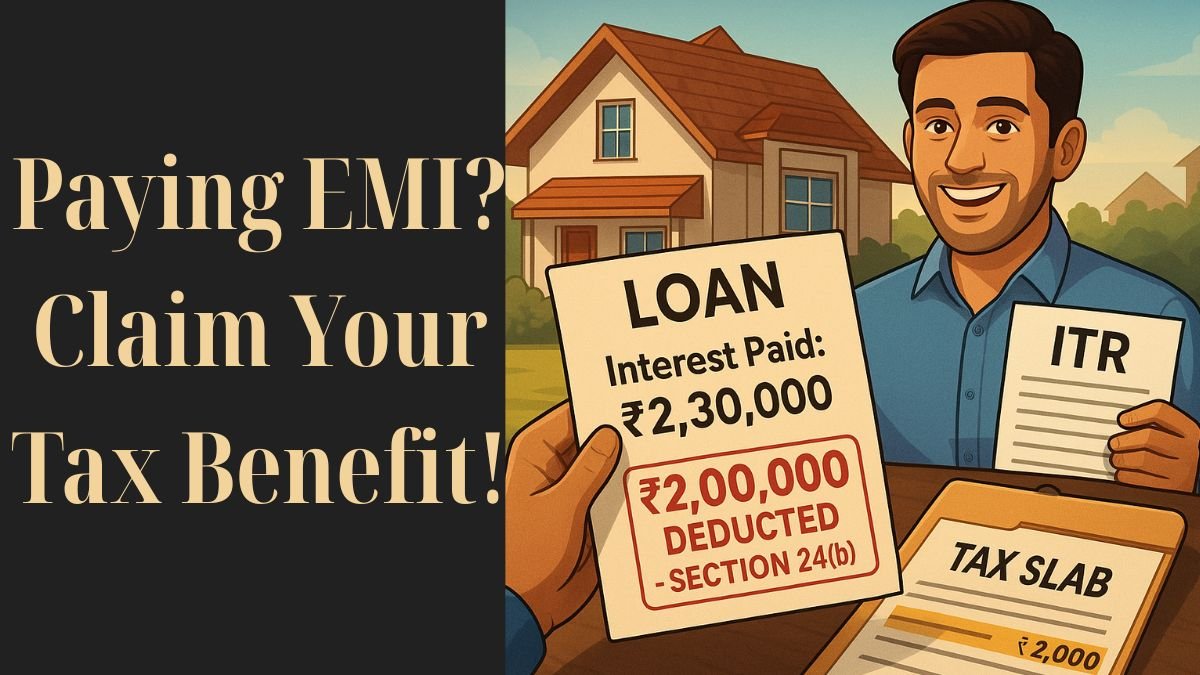

Under Section 24(b) of the Income Tax Act, you are allowed to claim a deduction up to ₹2 lakh against the interest paid on your home loan, provided the house is self-occupied.

Let’s break it down:

- Self-occupied property: Maximum deduction allowed = ₹2,00,000 per financial year.

- Let-out property: No upper limit on interest, but loss under “Income from house property” can be adjusted only up to ₹2 lakh against other income.

Key Conditions for Section 24b Deduction

To avail of the full deduction of ₹2 lakh, the following conditions for Section 24b must be satisfied:

- The loan must be taken for the purchase or construction of a house property.

- Construction or purchase must be completed within 5 years from the end of the financial year in which the loan was taken.

- For under-construction properties, the deduction is limited to ₹30,000 if construction isn't completed in 5 years.

- Interest for the pre-construction period (before completion) can be claimed in 5 equal instalments, starting from the year of completion.

Section 24b for Let Out Property

In the case of a let-out property, there is no limit on the amount of interest you can claim under Section 24b of the Income Tax Act for let-out property. However, the total loss that can be set off under “Income from House Property” is restricted to ₹2 lakh per year. The rest is carried forward for 8 assessment years. "

Section 24b in the New Tax Regime

A common query is: Can I claim this deduction under the new tax regime?

Unfortunately, the deduction under Section 24b is NOT available if you opt for the new tax regime (Section 115BAC). So, if your home loan interest is substantial, it might be more beneficial to stick to the old regime.

Personal Loan for House Repairs?

Yes, you read that right. You can also claim a deduction under Section 24b for a personal loan, provided the funds are used for the repair, renovation, or reconstruction of house property. However, in this case, the limit is ₹30,000.

Section 24b vs Section 80EE/80EEA

Many taxpayers confuse Section 24b with Section 80EE or 80EEA, which are additional benefits available for first-time homebuyers.

Here’s a quick comparison:

|

Section |

Purpose |

Deduction Limit |

Type of Loan |

|

24(b) |

Interest on housing loan |

₹2,00,000 |

Any home loan |

|

80EE |

First home buyer (FY 2016-17) |

₹50,000 |

Loan sanctioned in FY16- 17 |

|

80EEA |

Affordable housing (up to ₹45 lakh) |

₹1,50,000 |

Loan sanctioned between Apr 2019–Mar 2022 |

How to Claim Deduction Under Section 24b

- Get a home loan interest certificate from your lender.

- Calculate the total interest paid during the financial year.

- Ensure your property construction is complete.

- Report the deduction under Schedule HP (House Property) in your ITR.

Real-Life Example

Let’s say Rahul took a home loan of ₹40 lakhs in 2021 at 8% interest. He pays around ₹3.2 lakh in annual interest.

- Since Rahul lives in the house, he can claim a maximum of ₹2 lakh under Section 24b.

- If he had rented it out, he could still claim the entire ₹3.2 lakh as a deduction (subject to the ₹2 lakh set-off rule). "

Final Words

Section 24b of the Income Tax Act is one of the most useful deductions for home loan borrowers. It empowers you to claim tax benefits on your home loan interest, & in some cases, even on personal loans used for house repairs.

To sum up:

- Deduction limit = ₹2,00,000 for self-occupied properties

- No limit for let-out properties (but ₹2 lakh inter-head set-off cap)

- Applicable only in the old tax regime

- Deduction allowed even for pre-construction interest

- Section 24(b) can be combined with Section 80C & 80EEA for higher tax savings

🏡 Need expert help with filing your ITR or claiming Section 24b deduction correctly?

Visit www.callmyca.com to book a session with a Chartered Accountant now.