India’s income tax system is based on the concept of “residence” & “source.” But what happens when a person is a non-resident yet earns income that’s somehow connected to India? That’s where Section 9 of the Income Tax Act steps in.

This section plays a pivotal role in determining the scope of income deemed to accrue or arise in India, especially for non-residents & foreign entities doing business or earning income from Indian sources.

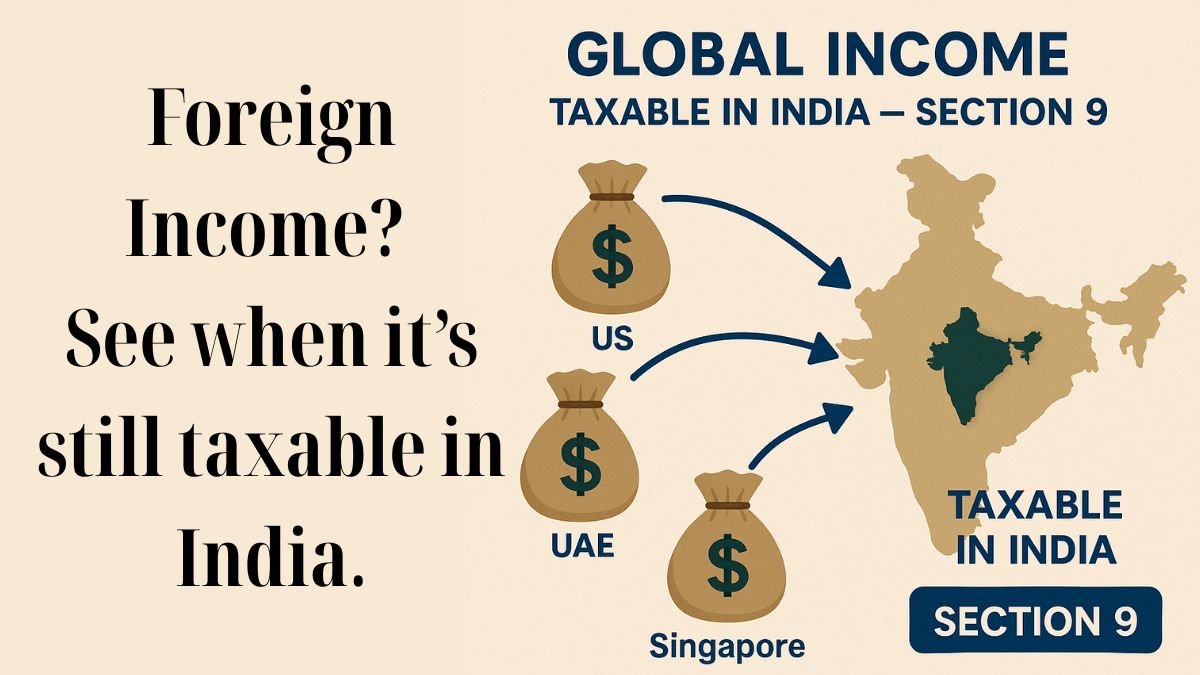

What Is Section 9 of the Income Tax Act?

Section 9 administers income deemed to arise or accrue in India. It brings into the Indian tax net those incomes that may not have been generated physically within India but have a close enough connection to be taxed here.

In simpler words, Section 9 of the Income Tax Act ensures that India rightfully taxes income that, while not entirely local, has an Indian linkage, such as royalty payments, interest, technical fees, and capital gains. "

Key Types of Incomes Covered under Section 9

- Income through or from a business connection in India

- Salaries paid by the Government of India to a citizen for services rendered outside India

- Dividend income from Indian companies

- Interest and royalty income from Indian sources

- Technical service fees received from an Indian entity

These categories define income deemed to accrue or arise in India, ensuring that any non-resident receiving such income is taxed accordingly. "

Why Is This Important for NRIs and Foreign Businesses?

Section 9 is one of the fundamental provisions relevant for a non-resident’s tax exposure. Suppose an NRI receives interest from an Indian bank, or a foreign company receives fees for technical services from an Indian client. Even if they are not physically in India, this income may be deemed to accrue or arise in India & become taxable.

This is particularly critical in today's global economy, where businesses & individuals interact across borders. Knowing how Section 9 determines the scope of income deemed to accrue or arise in India helps avoid non-compliance and unnecessary tax liabilities.

Example for Better Understanding

Let’s say a UK-based software company provides technical support services to an Indian IT firm and receives fees. Even though the work was performed entirely in the UK, the payment originates from India & is related to Indian business activity. Therefore, under Section 9, this payment could be deemed to accrue or arise in India & hence be taxable in India.

Final Thoughts

Section 9 of the Income Tax Act is a powerful provision that extends India’s taxation authority beyond its borders by linking income to Indian sources. Whether you're a non-resident earning royalties from India or a foreign company providing consultancy services, this section may apply to you.

If you're unsure how this affects your tax situation, consult a tax advisor or CA to avoid surprises during assessments.