When it comes to tax-saving strategies, businesses often overlook a key component: the provision for gratuity. This is where Section 40A(7) of the Income Tax Act comes into play. Far more than just a regulation on claiming gratuity expenses, this section determines whether your business qualifies for a deduction or ends up facing a higher tax burden. For companies aiming to stay compliant & optimise their tax liabilities, understanding this provision is no longer optional—it's essential.

What is Section 40A(7)?

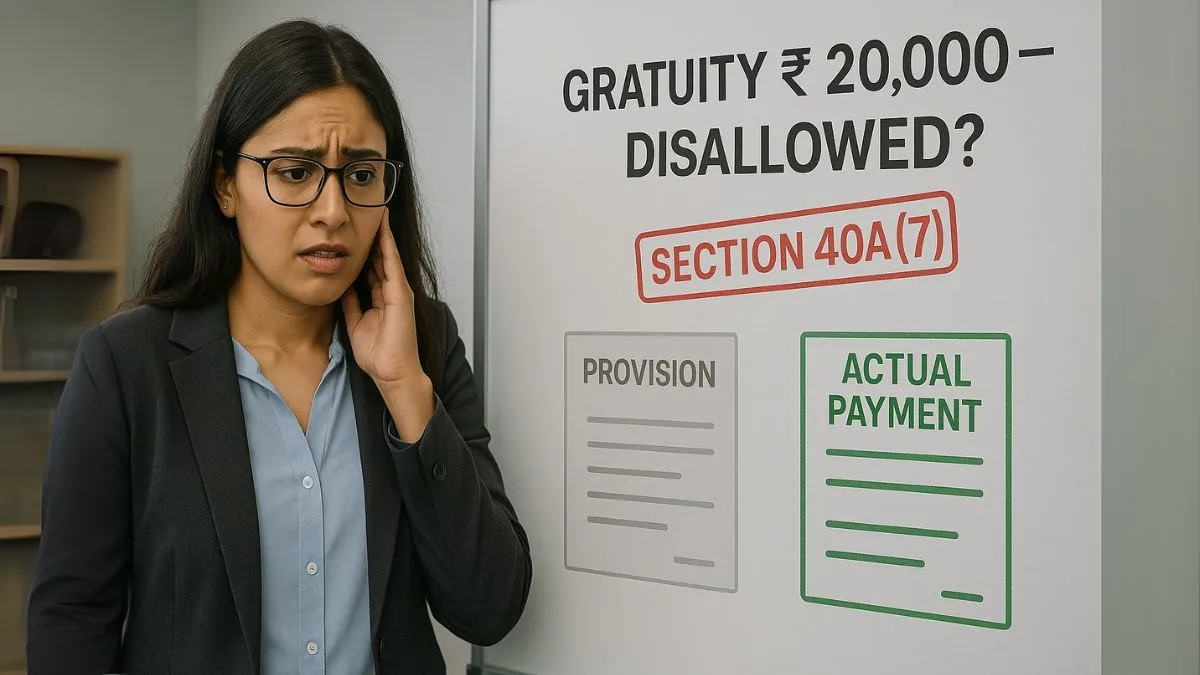

Section 40A(7) deals with one specific scenario—gratuity payments made by businesses to employees. But there’s a catch. You can’t just make a provision in your books & claim that amount as an expense to reduce taxable income. The law is crystal clear: provisions for gratuity are allowed as a deduction only under certain conditions.

Let’s decode those conditions in a way that makes sense.

What the Law Says

Under Section 40A(7), any provision for gratuity will be disallowed unless it meets these two criteria:

- It must be made for the payment of a gratuity that becomes payable during the financial year.

- The provision should be backed by an approved gratuity fund, & actual contributions must be made to that fund before the due date of filing the return.

So, making a journal entry in the books is not enough. If you haven’t contributed to a recognised gratuity fund, that amount will be disallowed as an expense."

Why Simply Making a Provision Won’t Help

Many businesses tend to pass year-end entries for gratuity, hoping to save tax. But unless that provision is backed by payment to an approved gratuity fund, Section 40A(7) kicks in & blocks the deduction. This often results in higher taxable profits & leads to unnecessary tax liabilities. Imagine making an expense on paper, only to find out the taxman won’t allow it!

Gratuity Obligations for Employers

Gratuity is not just a financial liability. It’s a statutory obligation under the Payment of Gratuity Act, 1972. Businesses with 10 or more employees are bound by it. When an employee completes five years of continuous service, gratuity becomes payable.

That’s why many smart companies set up approved gratuity funds through LIC or other insurers. This ensures they’re not just complying with labour laws but also qualifying for tax benefits under Section 40A(7). Without such a setup, even legitimate gratuity provisions won’t reduce your taxable income.

Example to Break It Down

Suppose XYZ Pvt. Ltd. makes a gratuity provision of ₹5 lakhs in FY 2024–25. However, it doesn’t contribute this amount to any approved gratuity fund. At the time of filing ITR, the tax officer disallows this ₹5 lakh under Section 40A(7). The result? Taxable income increases by ₹5 lakh, increasing the company’s tax burden by over ₹1.25 lakh (assuming a 25% tax rate).

Now flip the scenario. XYZ contributes this ₹5 lakh to a LIC-approved gratuity fund. The deduction is allowed. That’s tax optimisation done right."

Summary Table

|

Particulars |

Allowed as Deduction? |

|

Provision made without payment |

❌ No |

|

Provision backed by actual fund contribution |

✅ Yes |

|

Entry passed in books only |

❌ No |

|

The fund was approved by the authorities |

❌ No |

|

Contribution to approved gratuity fund |

✅ Yes |

What Happens If You Violate Section 40A(7)?

- Tax disallowance increases your taxable income.

- You could be liable for a penalty & interest.

- Your tax audit may flag the discrepancy.

- It may affect your credit rating if overstated profits are corrected later.

The easiest way to avoid this? Start an approved gratuity fund, make actual contributions annually, & never rely on just book entries.

Expert Insight

Section 40A(7) is part of a broader framework in the Income Tax Act that stops businesses from claiming unreal expenses. Like its cousin Section 43B (which applies to actual payments like PF, ESI, etc.), this section exists to ensure only real, money-backed outflows are deducted. That’s why tax consultants constantly advise reviewing gratuity accounting entries before finalising books.

✅ Final Words

Gratuity isn’t just about employees—it’s about smart tax planning. And Section 40A(7) ensures that only the genuine provisions get the benefit. It’s a perfect example of how compliance & savings can go hand in hand—if you understand the law correctly.

Want to set up an approved gratuity fund, clean up your books, or ensure your expenses don’t get disallowed under Section 40A(7)?

Let our expert chartered accountants at Callmyca.com help you do it right—we’ll keep your tax strategy bulletproof.