What Is Tax Year in India? Meaning, Period & Income Tax Act 2025 Explained

“What is tax year?”

You’ve probably seen this question a hundred times. And yet, the confusion never really goes away.

Because earlier, India had two terms — Financial Year and Assessment Year. Two different meanings. Two timelines. Slightly confusing.

Now, the framework is evolving.

Under the revised approach, the concept of a Tax Year is intended to be more streamlined and easier to interpret.

So, what exactly is a Tax Year?

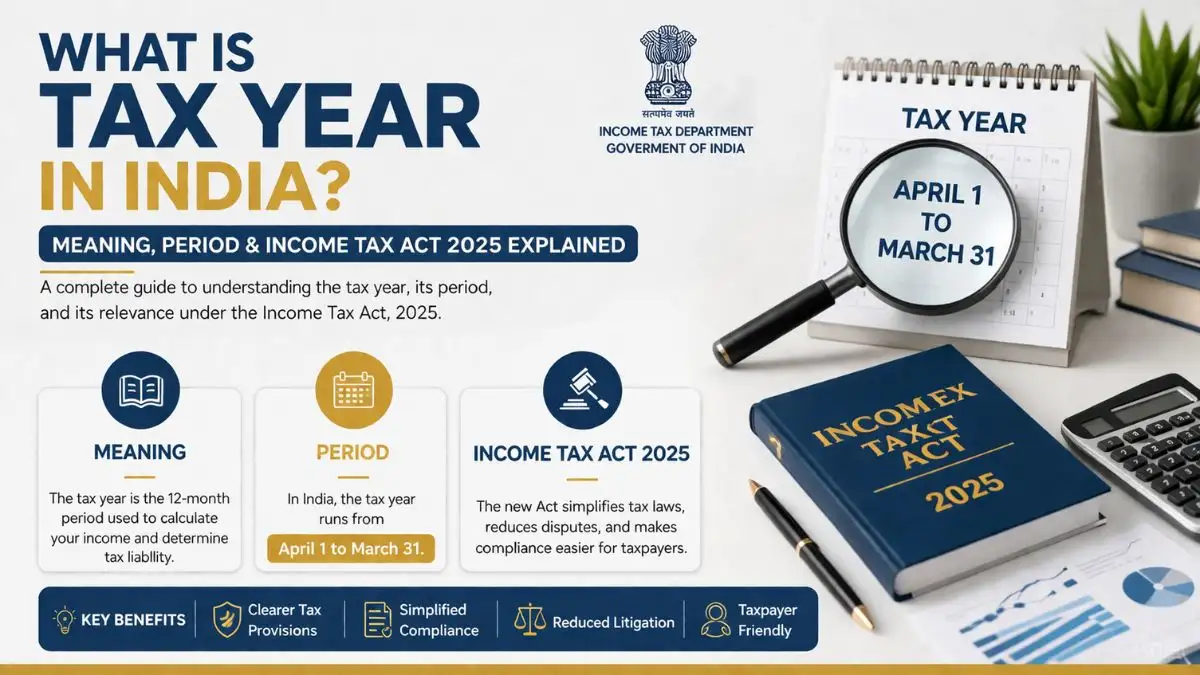

A Tax Year is basically a 12-month period that starts on April 1 and ends on March 31 of the following year.

In India, The Indian tax year is from 1 April to 31 March. This period is where all your income gets counted, tracked, and eventually taxed.

Earlier, this same year was divided into two concepts:

- Financial Year (when income is earned)

- Assessment Year (when it is taxed)

Now, the new system aims to merge both into one single Tax Year.

What changed under the Income Tax Act 2025?

In the Income Tax Act 2025 (enforced on April 1, 2026), the term "Tax Year" refers to the unified 12 months period that begins on April 1 and ends on March 31, taking place of the previous two terms, "Financial Year" (FY) and "Assessment Year" (AY).That means:

- No more confusion between FY and AY

- One single year for earning and taxation

- Easier understanding for taxpayers

Honestly, this was needed.

Because most people never really understood the difference between FY and AY anyway.

Why does a Tax Year exist at all?

Now think about this.

Why do we even need a Tax Year?

Why not just calculate tax randomly whenever income happens?

Because there needs to be a structured period.

A fixed timeline where:

- Income is recorded

- Expenses are tracked

- Tax liability is calculated

Tax Year means the 12-month period beginning on 1 April and ending on 31 March.

And during this time, everything related to your income gets documented.

What does “annual accounting period” actually mean?

“an annual accounting period for paying or withholding taxes”

This is the time frame used to:

- Record your income

- Maintain financial records

- Calculate taxes

In fact, a Tax Year is also an annual accounting period for keeping records and reporting income and expenses.

So whether you’re a salaried employee, business owner, or freelancer — this period defines your financial activity.

One important line people often misunderstand

“A tax year is the assessment year and the financial year.”

This statement was partially true earlier — when both existed separately.

But under the new system, the Tax Year merges both concepts into one.

So instead of two timelines, you now have one unified year.

Why April to March?

Why not January to December like many other countries?

The reason is historical and administrative.

India follows a fiscal system aligned with government budgeting cycles. Starting from April allows better planning for revenue and expenditure.

So yes, the The Indian tax year is from 1 April to 31 March.

And this structure is likely to stay.

Common confusion people still have

Even after simplification, people ask:

- “Which tax year am I filing for?”

- “Is it current year or previous year?”

- “Does income belong to this year or next?”

All of this confusion comes from mixing old concepts with the new Tax Year system.

Once you understand that everything revolves around one fixed 12-month period, things become much clearer.

What actually happens during a Tax Year?

During a Tax Year, multiple things happen:

- You earn income

- Taxes may be deducted (TDS)

- You maintain records

- You track expenses or deductions

And at the end of this period, your total income is calculated for taxation.

Small detail… but very important

Most people overlook this.

Your tax planning should also follow the Tax Year.

Not calendar year.

Because deductions, exemptions, and investments are all calculated within this specific year.

If you miss that timeline, you can’t go back and fix it later.

Final thought

Once you understand that it’s simply one year beginning on April 1st and ending on March 31st of the following year, things will be easier for you from there on out.

It is always better for you to clear up any confusion about your finances, paperwork, or filing in a specific time period.

There are sites such as Callmyca.com where you will receive practical assistance in understanding the concept.