In India, valuing unquoted or unlisted shares has always been a sensitive issue. Unlike shares of listed companies, which have a clear market price, privately held shares often have no visible benchmark. This opens doors to manipulation — or at least the appearance of manipulation — especially when shares are transferred at very low prices.

To protect revenue & curb potential misuse, the government introduced Section 50CA, a rule designed to ensure the fair market value (FMV) becomes the basis of taxation, not the artificially low transfer price.

In simple terms:

Section 50CA is a special provision that addresses the undervaluation of unquoted shares during a transfer. It aims to prevent tax evasion by ensuring that capital gains are calculated based on FMV rather than a lower transaction price.

What Is Section 50CA of the Income Tax Act?

The law that insists on “real value” over “sale value”

Section 50CA is titled: “Special provision for full value of consideration for transfer of share other than quoted share.”

This means it applies only to:

- Unlisted shares

- Unquoted shares

- Shares without a market-driven price

Under this rule:

If the sale price of an unquoted share is less than its fair market value, then — for tax purposes — FMV is treated as the full value of consideration.

So even if you sell a share for ₹10, but FMV is ₹40, your capital gains will be calculated using ₹40.

Also Read: Valuation of Shares for Angel Tax and Income Tax Compliance

Why Section 50CA Was Introduced

Before this section existed, companies could:

- Sell shares at very low prices

- Transfer ownership quietly

- Avoid capital gains

- Move funds under the radar

- Create unfair losses to reduce taxes

In fact, I remember a case where a company’s shares were transferred between related parties for a token amount — just ₹1 per share — while the business was worth crores. Transactions like this triggered red flags, and Section 50CA was created precisely to close such loopholes.

Its purpose is simple but powerful: Prevent the undervaluation of unquoted shares during their transfer.

How FMV Is Calculated for Section 50CA

FMV is determined using specific methods prescribed under Rule 11UA. This rule considers:

- Net asset value

- Liabilities

- Book value adjustments

- Market-based valuation

- Merchant banker valuation (in some cases)

This ensures the value is not arbitrary but grounded in defined formulas.

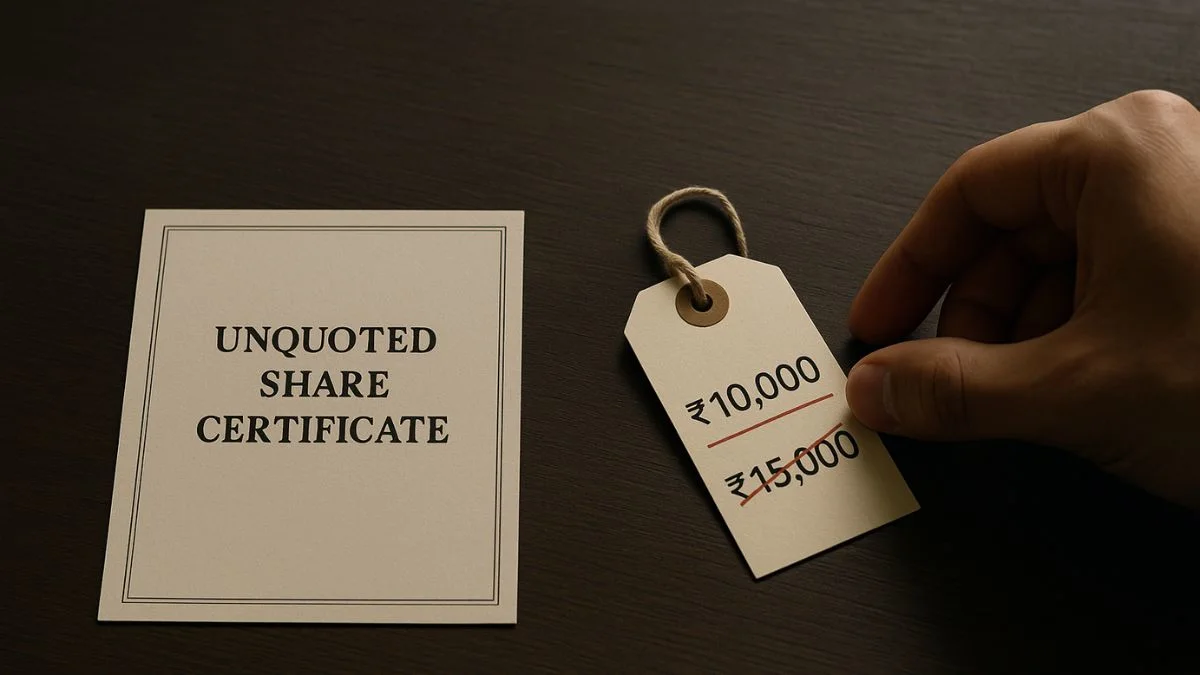

A Simple Example to Understand Section 50CA

Imagine you own shares of a private company. A buyer wants to purchase them for ₹500 per share. But valuation under Rule 11UA shows:

FMV = ₹900 per share

Even though you sell for ₹500, the Income Tax Act will treat:

- ₹900 as the total value of consideration for non-quoted shares"

- And your capital gains will be calculated using ₹900

This is the heart of Section 50CA.

Who Has to Pay the Tax?

Section 50CA applies to the seller, not the buyer. So if you are transferring unlisted shares:

- At a lower price

- To a related person, or

- To an independent buyer

— you still owe tax based on FMV.

Also Read: The Hidden Formula Behind Fair Market Value: What Rule 11U Really Reveals

When Section 50CA Does Not Apply

The government recognises that genuine situations may require selling shares below FMV.

So exemptions have been given when:

- The transfer is part of an approved restructuring

- Shares are transferred under IBC (Insolvency & Bankruptcy Code)

- The Central Government notifies specific cases

- Valuation mismatch is due to regulatory restrictions

These exceptions ensure that businesses going through distress or restructuring aren’t burdened unfairly.

Why Section 50CA Matters for Businesses

If you are:

- A startup founder

- A shareholder in a family-owned business

- An investor exiting a private company

- A promoter re-structuring ownership

…Section 50CA directly affects you.

It protects the integrity of share transfers & ensures that capital gains reflect the true value of the transaction.

A founder once shared with me,

“I sold my shares cheaply because I needed the money. But Section 50CA still made me pay tax on FMV — that’s when I realised valuation isn’t just a formality.”

That’s the emotional weight this section carries.

Common Mistakes Taxpayers Make

- Assuming FMV doesn’t matter if buyer & seller agree on a price

- Ignoring valuation rules

- Not obtaining merchant banker reports when required

- Selling shares informally without paperwork

- Believing Section 50CA applies only to large companies

- Confusing FMV with book value

A little awareness goes a long way in avoiding unnecessary tax burdens.

Also Read: A Deep Dive into Charitable and Religious Income Exemptions

Key Takeaways About Section 50CA

- Section 50CA is a special provision for undervalued transfers of unquoted shares.

- It applies when the sale price is lower than FMV.

- The law treats FMV as the full value of consideration for tax calculation."

- It protects against undervaluation & potential tax evasion.

- FMV is determined through Rule 11UA valuation methods.

- Exemptions exist for restructuring, IBC cases, and government-notified situations.

Conclusion

Section 50CA is one of those tax rules that quietly ensures fairness in India’s financial ecosystem. By insisting on FMV for taxing transfers of unquoted shares, it closes loopholes & keeps valuations transparent. Whether you’re part of a private company, a startup, or a family business, understanding this section helps you make informed decisions during any share transfer.

If you ever need help with valuation reports, tax planning, or understanding how Section 50CA affects your transaction, the experts at CallMyCA.com are always here to guide you with clarity and confidence.