Section 156 of Companies Act 2013: DIN Intimation Rules

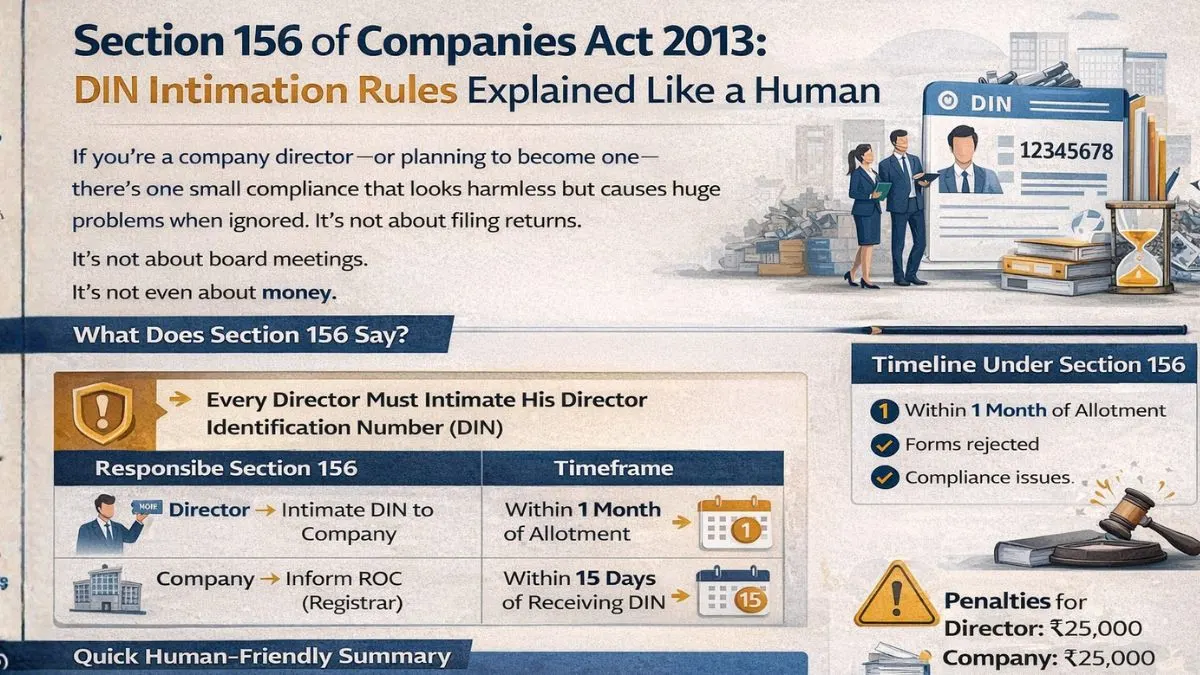

If you’re a company director—or planning to become one—there’s one small compliance that looks harmless but causes huge problems when ignored.

It’s not about filing returns.

It’s not about board meetings.

It’s not even about money.

It’s about DIN.

And the law that governs this is Section 156 of the Companies Act 2013.

What Is Section 156 of the Companies Act 2013?

In simple words, section 156 of the Companies Act 2013 says:

👉 Every director must inform (intimate) his Director Identification Number (DIN)

👉 to the company or companies where he is a director

👉 within one month of receiving the DIN from the Central Government

That’s it.

This section exists to ensure:

- transparency

- correct identification of directors

- proper MCA records

Why DIN Intimation Is So Important

Think of DIN as

A permanent Aadhaar number for directors.

Once allotted, it stays with you for life.

But here’s the key point many people miss:

Just getting a DIN is not enough.

The company must officially know that:

- this DIN belongs to this director

That’s why Section 156 lays down the requirement for all existing directors to inform the company about their DIN.

Who Is Covered Under Section 156?

Section 156 of the Companies Act 2013 applies to:

- Newly appointed directors

- Existing directors who receive DIN later

- Directors holding positions in multiple companies

The law is very clear:

Every existing director shall intimate his DIN to the company.

This is a personal responsibility of the director.

What Does “Intimate His Director Identification Number” Mean? Mean?

This is where confusion usually starts.

To intimate his Director Identification Number means:

- Officially informing the company

- In writing

- In the prescribed manner

It is not enough that:

- the director assumes the company already knows

- the DIN is mentioned in some old document

Formal intimation is mandatory.

Timeline Under Section 156 (Very Important)

Let’s talk dates—because penalties depend on timelines.

Timeline for Director

Under section 156 of the Companies Act 2013:

- The director must intimate his DIN

- Within one month of receiving it from the Central Government

This timeline is strict.

Timeline for Company

Once the company receives the intimation from the director:

Every company shall, within fifteen days of the receipt of intimation under section 156,

inform the Registrar of Companies (ROC)

This is usually done by filing the prescribed e-form.

So Section 156 creates a two-step compliance:

- Director → Company

- Company → ROC

Why the Law Splits Responsibility

This is intentional.

The law wants:

- directors to take ownership of their DIN

- companies to maintain accurate MCA records

So both sides are accountable.

Practical Example (Real-Life Situation)

Let’s take a very common scenario.

Example 1: New Director Appointment

- Mr. A applies for DIN

- DIN is allotted on 1st August

- Mr. A becomes director in 2 companies

Under Section 156 of the Companies Act 2013:

- Mr. A must intimate his DIN to both companies by 31st August

- Each company must then inform ROC within 15 days

If either step is missed, there is non-compliance.

Example 2: Director Already on Board, DIN Received Later

Sometimes:

- The director was appointed earlier

- DIN was applied for later

Still:

Every existing director shall intimate his DIN to the company

No exceptions.

What Happens If Section 156 Is Not Complied With?

This is where things turn unpleasant.

Consequences for Director

If a director fails to intimate DIN:

- Penalty can be imposed

- The director may face compliance issues

- Future filings may get blocked

Consequences for Company

If the company fails to inform ROC:

- Company is liable for penalties

- MCA records remain incomplete

- Compliance rating may be affected

That’s why ignoring Section 156 is never a good idea.

Is This Requirement Just a One-Time Compliance?

Mostly yes—but with a catch.

DIN intimation is required:

- when DIN is first received

- when director joins a new company

So if you become director in another company:

- you must again intimate his Director Identification Number to that company

Section 156 vs Other DIN-Related Sections (Quick Clarity)

Many people mix up DIN sections.

Here’s a simple distinction:

- Section 152 → Appointment of directors

- Section 153 → Application for DIN

- Section 154 → Allotment of DIN

- Section 156 → Director to intimate DIN

- Section 157 → Company to inform ROC

So Section 156 is specifically about intimation by the director.

Common Mistakes Directors Make

From real-world experience, these mistakes are very common:

- Assuming the CA or CS will do everything

- Missing the 1-month deadline

- Not intimating DIN to all companies

- Confusing DIN allotment with DIN intimation

- Delaying company filing after intimation

Most of these happen due to lack of awareness, not intention.

Best Practices to Stay Compliant

Here’s what actually works:

For Directors

- Intimate DIN immediately after allotment

- Keep written proof of intimation

- Track companies where you are a director.

For Companies

- Record DIN intimation properly

- File ROC form within 15 days

- Maintain updated director records

This avoids penalties and future headaches.

Why Section 156 Exists (The Bigger Picture)

The government introduced DIN to:

- track individuals acting as directors

- prevent misuse of multiple identities

- improve corporate transparency

Section 156 of the Companies Act 2013 ensures that:

DIN is not just allotted but properly linked to the right companies.

Section 156 in One Simple Line

If you remember only one thing, remember this:

Section 156 of the Companies Act 2013 requires every director to inform the company of his DIN within one month and the company to inform the ROC within 15 days.

That’s the entire section in one sentence.

Quick Human-Friendly Summary

- Section 156 of Companies Act 2013 deals with DIN intimation

- Every director must intimate his DIN to the company

- This must be done within one month of receiving DIN

- Every existing director shall intimate his DIN to the company

- Every company must inform ROC within 15 days

- Non-compliance attracts penalties

- It ensures transparency and accurate MCA records

Final Thoughts (Real Talk)

Section 156 is not complicated.

But it’s one of those compliances where:

“Chhoti si delay, bada issue ban jaata hai.”

DIN is your identity as a director.

If that identity is not properly recorded, everything else becomes messy.

If you’re a director—or planning to become one—make sure Section 156 of the Companies Act 2013 is complied with on time. It saves you penalties, notices, and unnecessary stress.

And if you want help with DIN compliance, ROC filings, or director-related matters, having the right professional support makes the process smooth and worry-free.

For expert assistance with Companies Act compliances, visit callmyca.com.