Income from House Property (22 to 27)

Are you an owner of a house, flat, or building in India? Have you ever scrolled through income from house property—sections 22-27—while filing your ITR or trying to comprehend why you need to pay taxes even if you hadn't received the rent amount just because you own the building?

And that confusion is very common.

Property income under the Income Tax Act doesn’t work the way most people assume it does. It’s not just about rent received. It’s about ownership, annual value, deductions, and legal assumptions made by law.

Sections 22 to 27 of the Income Tax Act, 1961, together form a complete code that decides:

- When property income is taxable

- In whose hands it is taxable

- How much is taxable

- What deductions are allowed

What is "Income from House Property"?

Under the Income Tax Act:

Income from house property—income arising from ownership of a building or land appurtenant thereto.

It is the word "ownership" here, not "rent."

That’s why:

- Even self-occupied property is considered

- Even vacant property can be taxable

- Even deemed ownership is taxed

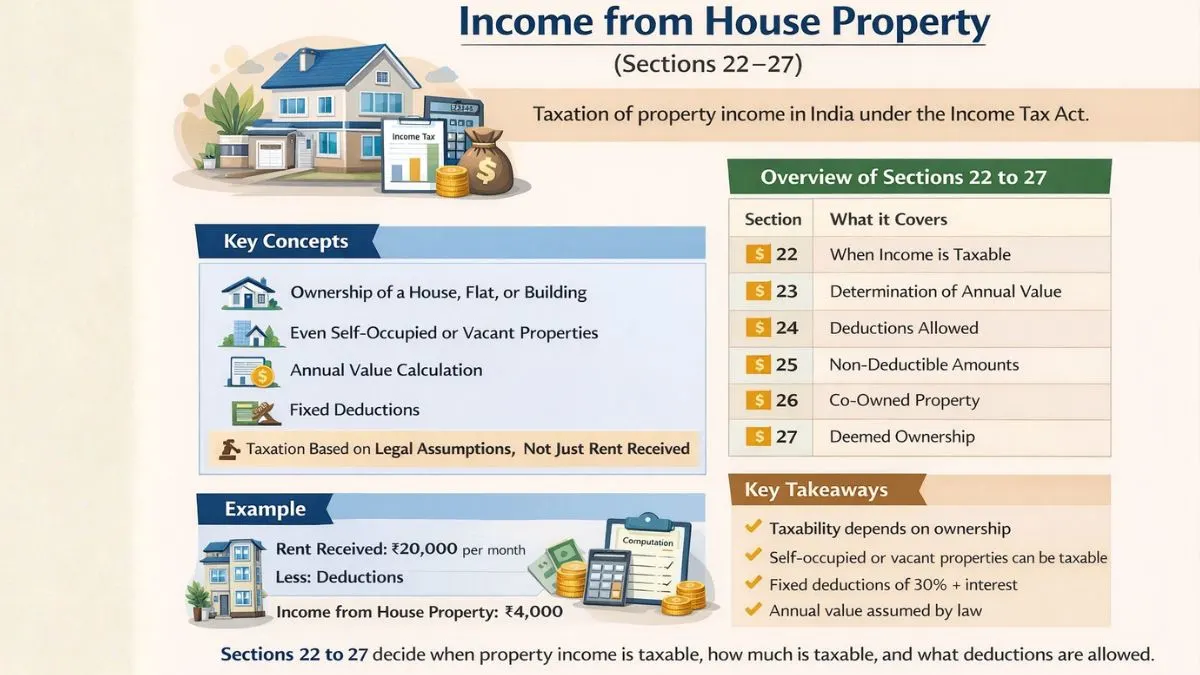

Overview: Sections 22 to 27 at a Glance

|

Section |

What it Covers |

|

Section 22 |

Chargeability of income from house property |

|

Section 23 |

Determination of annual value |

|

Section 24 |

Deductions from house property income |

|

Section 25 |

Amounts not deductible |

|

Section 26 |

Property owned by co-owners |

|

Section 27 |

Deemed ownership |

Together, these sections decide how property income is computed.

Section 22 – When Is Income From House Property Taxable?

Section 22, income from house property, is the charging section.

It states:

The annual value of property consisting of any buildings or land appurtenant thereto shall be taxable in the hands of the owner.

Important Points Under Section 22

- Property must be building or land attached to a building.

- The owner must be legal or deemed the owner.

- Property should not be used for owner’s business or profession

If property is used for business:

👉 Income is taxed under business income, not house property.

What Is NOT Covered Under Section 22

The following are excluded:

- Vacant land (without building)

- Property used for own business

- Rental income from subletting (taxed as other sources)

This distinction is critical during assessments.

Section 23 – Determination of Annual Value

This is where most income from house property problems and solutions arises.

Section 23 determines how much income is assumed from property—even if you didn’t earn that much.

What Is Annual Value?

Annual value is the reasonable expected rent of the property for one year.

It can be:

- Actual rent received or receivable

- Expected rent

- Nil (in some cases)

Types of House Property Under Section 23

1. Self-Occupied Property (SOP)

- Used for own residence

- Annual value = Nil

- A maximum oftwo self-occupied properties allowed

Earlier it was one; now two are permitted.

2. Let-Out Property

- Given on rent

- Annual value = Actual rent or expected rent, whichever is higher

This is fully taxable (after deductions).

3. Deemed Let-Out Property

- Property not rented but not self-occupied

- Annual value calculated as if rented

Many people get notices due to this concept.

Vacant Property and Section 23

If property:

- Is intended to be let out

- Remains vacant for some time

Then:

- Actual rent received is considered

- Expected rent is ignored for vacancy period

This offers relief—but only if the intention to let out is proven.

Section 24 – Deductions From House Property Income

This is the most taxpayer-friendly section.

Section 24 allows flat deductions, regardless of actual expenses.

Section 24(a) – Standard Deduction (30%)

- Flat 30% deduction

- On Net Annual Value

- Allowed without any proof

This covers:

- Repairs

- Maintenance

- Painting

- Brokerage

Even if you spent nothing, 30% is allowed.

Section 24(b) – Interest on Housing Loan

Interest on borrowed capital is allowed.

Limits:

- Self-occupied property: ₹2,00,000

- Let-out property: No limit (but overall loss cap applies)

Interest deduction is one of the biggest tax benefits for homeowners.

Loss From House Property – Important Rule

If deductions exceed income:

- Loss is generated

But:

- The maximum set-off against other income is ₹2,00,000

- Balance loss carried forward for 8 years

This is a common area of scrutiny.

Section 25 – Amounts Not Deductible

Section 25 clarifies what you cannot deduct, such as:

- Personal expenses

- Capital repayment

- Municipal taxes not actually paid

This section prevents double or excessive claims.

Section 26 – Co-Owned Property

If property is owned by:

- Two or more persons

- With definite shares

Then:

- Income is taxed separately in each owner’s hands

- Section 22–24 applied individually

This helps co-owners claim separate deductions.

Section 27 – Deemed Ownership

This section answers:

Who is considered the owner for tax purposes—even if not the legal owner?

Under Section 27, deemed owner includes:

- Transferor under inadequate consideration

- Holder of impartible estate

- Member of cooperative society

- Person in possession under part performance (Section 53A TPA)

This prevents tax avoidance through legal structuring.

Income From House Property—

Example

Mr. A owns a flat:

-

Rent Received: ₹20,000 per month

Annual rent: Rs.

Municipal tax paid: ₹20,000

The amount of interest accrued on the loan

ComputationGross Annual Value: ₹2,40

Less Municipal Tax: ₹20,000

Net Annual Value: 2,20

Less 30% deduction:

₹

Less Interest: ₹1,Income from house property = Rs. 4,000

Thus, we have seen the process in which all three sections function together—that is,

Common Mistakes Taxpayers Make From the experience gained so far, the mistakes identified below are frequent:

- Treating second house as self-occupied incorrectly

- Ignoring deemed let-out concept

- Claiming full interest set-off wrongly

- Not declaring co-owner shares properly

- Confusing rent received with taxable income

Most notices arise from these errors.

Income From House Property Notes – Key Takeaways

- Taxability depends on ownership

- Rent is not the only factor

- Annual value is legally assumed

- Deductions are fixed, not actual

- Deemed ownership is taxable

- Loss set-off has limits

Once these concepts are clear, property taxation becomes predictable.

Why Sections 22 to 27 Are Interconnected

You cannot apply one section in isolation:

- Section 22 decides taxability

- Section 23 fixes value

- Section 24 gives relief

- Section 26 allocates income

- Section 27 decides ownership

Missing even one leads to wrong computation.

Income From House Property vs Business Income

Sometimes property income is taxed as business income if:

- Property is stock-in-trade

- Leasing is main business

- Complex commercial activities exist

But this depends on facts, not labels.

Sections 22 to 27 in One Simple Line

If we simplify income from house property section 22 to 27 in one sentence:

These sections decide when property income is taxable, how much is taxable, and what deductions are allowed.

Final Thoughts: Property Income Is About Law, Not Cash Flow

Many taxpayers say:

“But I didn’t receive rent!”

Income from house property is based on legal ownership and potential, not just cash received.

Once you understand Sections 22 to 27:

- Filing becomes easier

- Notices reduce

- Planning improves

Need help with property income computation, housing loan benefits, or ITR filing?

Visit callmyca.com for clear, practical guidance on income tax and property taxation.