Income Tax Section 234A: Why Filing Your ITR Late Always Costs You

Let’s be honest.

Almost everyone has said this at least once:

“We’ll file the return later… what difference will it make?”

And then, when the ITR is finally filed, you notice an extra amount added under interest.

No notice.

No warning.

Just extra tax to pay.

That silent charge usually comes from Income Tax Section 234A.

This section doesn’t care why you were late.

It only cares that you were late.

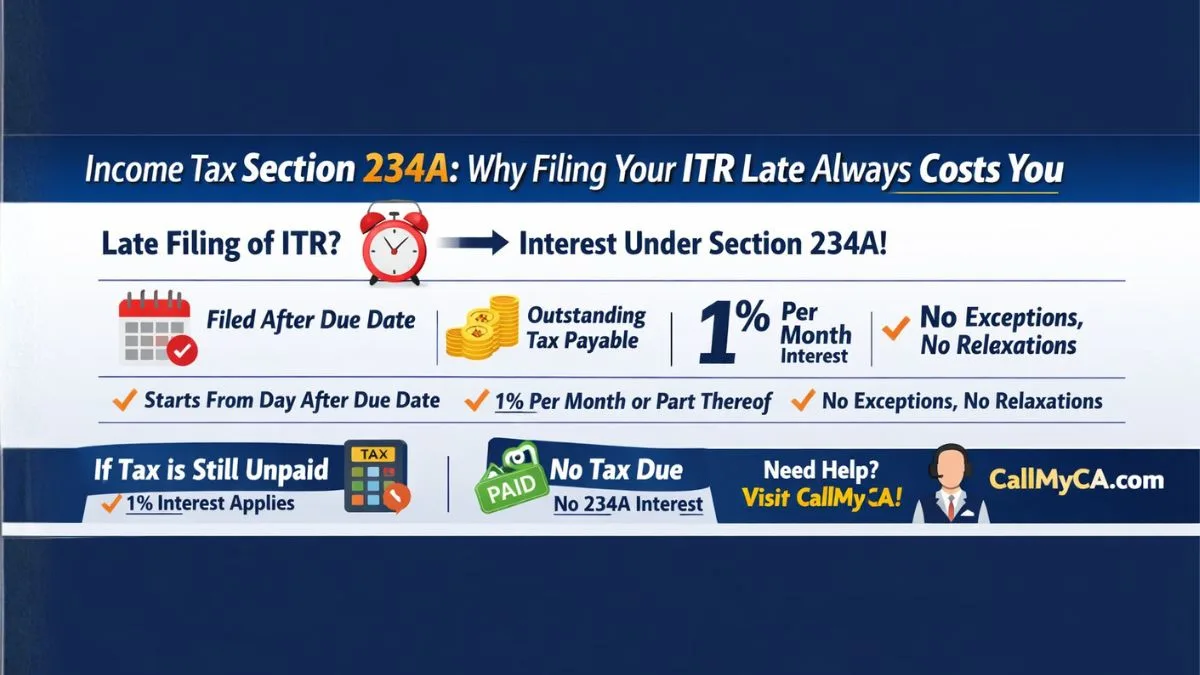

What Is Income Tax Section 234A?

In very simple words, income tax section 234a:

👉 imposes simple interest on taxpayers who file their Income Tax Return (ITR) after the due date

That’s it.

If your return is late, interest applies.

No discretion.

No negotiation.

That’s why the law clearly states:

It provides for levy of interest on account of default in furnishing return of income.

When Does Section 234A Apply?

Section 234A applies only in one situation:

👉 Late filing of your income tax return

If:

- you miss the due date, and

- you still have some tax payable

Then interest under section 234A becomes mandatory.

Does It Apply to Everyone?

Not exactly.

Income tax section 234a applies only if:

- your return is filed after the due date, and

- there is outstanding tax payable

If:

- you filed late, but

- your entire tax was already paid

then Section 234A interest may not apply.

From Which Date Is Interest Calculated?

This is very important.

Under Section 234A:

- interest is calculated from the day after the due date

- up to the date you actually file the return

Even:

- one-day delay

- or part of a month

is counted as a full month.

Rate of Interest Under Section 234A

The rate is fixed and simple:

👉 1% per month or part of a month

No slab.

No variation.

No relaxation.

That’s why delaying ITR filing becomes expensive very quickly.

On What Amount Is Interest Charged?

Interest under income tax section 234a is charged on:

Tax payable after adjusting TDS, TCS, advance tax, and reliefs

In simple words:

- whatever tax is still unpaid

- attracts 1% monthly interest

Simple Example to Understand Section 234A

Let’s take a very common situation.

Example 1: Late Filing with Tax Due

- Due date of ITR: 31 July

- Actual filing date: 20 October

- Tax payable after TDS: ₹40,000

Delay:

- August, September, October → 3 months

Interest:

- ₹40,000 × 1% × 3 months = ₹1,200

That ₹1,200 is interest imposed under section 234A.

Example 2: Late Filing but No Tax Payable

- Entire tax already paid via TDS/advance tax

- Return filed late

Result:

- No Section 234A interest

- But late filing fee under another section may apply

So Section 234A is strictly about interest, not penalty.

Section 234A Is NOT a Penalty

This is a very common misunderstanding.

Income tax section 234a:

- does not punish you

- does not depend on officer’s discretion

It simply compensates the government for:

- delayed payment of tax

- delayed filing of return

That’s why it applies automatically.

Section 234A vs 234B vs 234C (Quick Clarity)

People often see all three together and get confused.

Here’s the simplest way to remember:

- Section 234A → late filing of ITR

- Section 234B → not paying enough advance tax

- Section 234C → delay in advance tax installments

You can be charged all three at the same time.

Common Situations Where Section 234A Applies

From real-life filings, these situations trigger it most:

- freelancers missing due dates

- salaried individuals with additional income

- people waiting for Form 16 for too long

- investors with capital gains

- taxpayers assuming “A one-month delay is acceptable / works fine.”

If tax is payable and the return is late, Section 234A applies.

Can Section 234A Be Avoided?

Yes. Very easily.

Here’s what actually works:

1. File Return Before Due Date

Even if calculations are approximate.

2. Pay Self-Assessment Tax Early

Interest stops once tax is paid.

3. Don’t Wait for Perfect Data

Minor revisions are allowed later.

4. Track Due Dates Seriously

One reminder can save thousands.

What If You File a Return After December 31?

Earlier, belated returns were allowed till December 31.

Even then:

- Section 234A interest continued till filing date

Late is late—interest doesn’t stop early.

Common Myths About Section 234A

Let’s clear a few quickly:

❌ “A one-month delay is acceptable.”

✔ No. Even one day counts as a full month.

❌ “Only a penalty will apply, not interest.”

✔ Interest applies independently.

❌ “If we revise the return later, the interest will be removed.”

✔ Wrong. Interest remains.

Quick Human-Friendly Summary

- Section 234A applies to late filing of ITR

- Interest rate: 1% per month or part thereof

- Charged on outstanding tax

- Starts from day after due date

- Automatic and mandatory

- Different from penalty and late fees

Final Thoughts (Real Talk)

Section 234A doesn’t look scary—but it’s sneaky.

You don’t feel it when you delay filing.

You feel it when you finally click Submit.

Most people don’t lose money because taxes are high.

They lose money because timelines are ignored.

Once you understand income tax section 234a, one thing becomes clear:

Filing on time is the cheapest tax-saving strategy.

If you need help with:

- timely ITR filing

- advance tax planning

- avoiding 234A, 234B, and 234C interest

Professional guidance can save both money and stress.

For practical, no-nonsense tax support, visit callmyca.com.