Nominal Account Section: Meaning, Rules, and Examples

If you’re studying accounting or running a business, there’s one topic that almost everyone finds confusing at first—nominal account.

You hear things like

- “Rent is a nominal account.”

- “Nominal accounts are closed every year.”

- “They show profit and loss, not assets.”

And suddenly it feels like accounting is a foreign language.

But here’s the truth:

Nominal accounts are actually the easiest accounts to understand—once someone explains them like a human being, not like a textbook.

So in this blog, let’s break down the nominal account section in a very practical, real-life way.

No complicated definitions.

No robotic language.

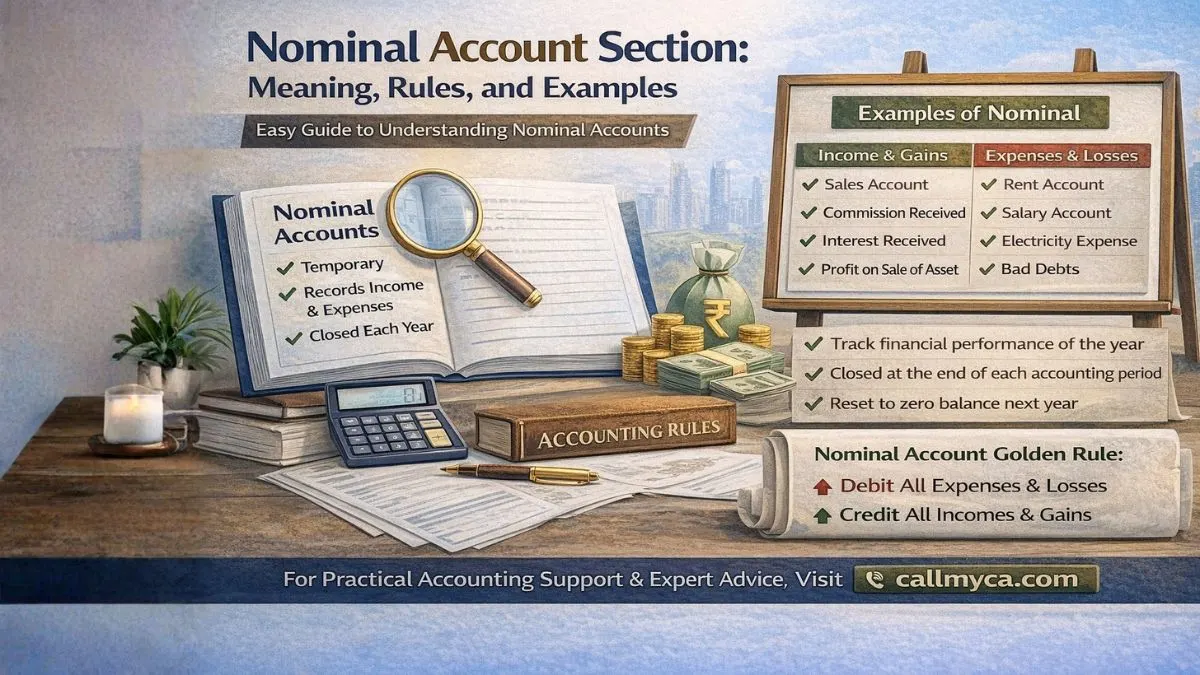

What Is a Nominal Account?

A nominal account is the part of the general ledger that records:

- Income

- Expenses

- Gains

- Losses

for a specific period of time, usually one financial year.

In simple words:

A nominal account tells you how much you earned or spent during the year.

Why Is It Called a “Nominal” Account?

The word “nominal” doesn’t mean “small” here.

It means:

- Temporary

- Period-based

- Not carried forward permanently

A nominal account is a part of the general ledger that is closed at the end of every financial or accounting year.

Once the year ends:

- Its balance becomes zero

- A fresh account starts next year

Nominal Account Section in the General Ledger

The nominal account section is the part of the general ledger that tracks a business’s:

- Expenses

- Losses

- Gains

- Revenues

for a particular accounting period.

That’s why nominal accounts are closely linked to:

- Profit & Loss Account

- Income Statement

They help answer one simple question:

“Did the business make a profit or loss this year?”

Key Characteristics of Nominal Accounts

Let’s clearly understand how nominal accounts behave.

1. Temporary in Nature

A nominal account holds its balance for an accounting period, usually one fiscal year.

After that:

- Balance is transferred to Profit & Loss Account

- Account is closed

2. Related Only to Income & Expenses

Nominal accounts:

- Do NOT show assets

- Do NOT show liabilities

They only record:

- Income earned

- Expenses incurred

- Gains and losses

3. Closed at the End of the Year

Nominal accounts are:

- The general ledger accounts that are closed at the end of each accounting year

This is one of their most important features.

Why Nominal Accounts Are Closed Every Year

This is a very common doubt.

Why not carry them forward like assets?

Because:

- Income and expenses belong to a specific time period

- Every year’s performance must be measured separately

Imagine mixing:

- Last year’s rent expense

- This year’s rent expense

You’d never know how the business performed this year.

That’s why a nominal account is a part of the general ledger that is closed at the end of every financial year.

Nominal Account Rule (Golden Rule)

Here’s the classic accounting rule for nominal accounts:

Debit all expenses and losses

Credit all incomes and gains

This single rule solves most journal entry confusion.

Examples of Nominal Accounts (Very Practical)

Let’s look at common real-life examples.

Expense Nominal Accounts

- Rent Account

- Salary Account

- Electricity Expense

- Telephone Expense

- Advertisement Expense

Yes—rent is a nominal account.

Income Nominal Accounts

- Sales Account

- Commission Received

- Interest Received

- Discount Received

Loss Nominal Accounts

- Loss on Sale of Asset

- Bad Debts

Gain Nominal Accounts

- Profit on Sale of Asset

- Compensation Received

All these are accounts that record income, expenses, gains, and losses.

Simple Journal Entry Example (Nominal Account)

Let’s say:

- You paid office rent of ₹10,000 in cash

Journal Entry:

Rent A/c Dr ₹10,000

To Cash A/c ₹10,000

Why?

- Rent = expense → Debit

- Cash = asset → Credit

This is how a nominal account records monetary transactions during a period.

Nominal Account vs Real Account (Quick Comparison)

This comparison clears a lot of confusion.

Nominal Account

- Records income & expenses

- Temporary

- Closed every year

- Shown in Profit & Loss Account

Real Account

- Records assets

- Permanent

- Carried forward every year

- Shown in Balance Sheet

That’s why people search for:

- “nominal account examples”

- “real account examples”

- “real account rule”

Where Do Nominal Accounts Appear in Final Accounts?

Nominal accounts appear in:

- Trading Account

- Profit & Loss Account

They do not appear in the balance sheet because they are closed.

So if you’re searching for:

“balance sheet account section”

Nominal accounts are not part of it.

Nominal Accounts and Financial Performance

Nominal accounts help answer questions like:

- Is the business profitable?

- Are expenses increasing?

- Is income stable?

Because they:

- Track financial transactions over a set period of time

- Reflect operational performance

This is why business owners should understand nominal accounts, not just accountants.

Common Mistakes Students Make with Nominal Accounts

From experience, these mistakes are very common:

- Treating rent as a real account

- Carrying forward expense balances

- Mixing income of two years

- Forgetting to close nominal accounts

Remember:

Nominal accounts are period-based, not permanent.

Why Nominal Accounts Matter for Business Owners

Even if you’re not an accountant, nominal accounts help you:

- Control expenses

- Analyse profit

- Budget better

- Understand where money is going

Every business decision starts with numbers—and nominal accounts tell that story.

Nominal Account Summary (One-Page Logic)

Let’s summarize everything simply:

- A nominal account records income, expenses, gains, and losses

- It is a type of account that is maintained to record monetary transactions

- It is used to keep track of financial transactions over a set period of time

- A nominal account holds its balance for one accounting year

- It is closed at the end of each financial year

- Examples include rent, salary, sales, commission, interest

- Rule: Debit expenses & losses, Credit incomes & gains

Final Thoughts

Nominal accounts aren’t difficult.

They’re just badly explained.

Once you understand that they:

- Measure performance

- Belong to one year only

- Reset every year

Accounting suddenly starts making sense.

If you’re a student, this clarity helps with exams.

If you’re a business owner, it helps decisions.

And if you want professional support with bookkeeping, accounting, or compliance—the right guidance can save you time and mistakes.

For practical accounting support and expert help, visit callmyca.com.