section 141(3) Of Companies Act 2013 – Auditor Disqualification

The place and the role of the auditor in the corporate world are unique. The auditor does not own the business, nor does he decide; he does not handle money, yet his simple sign-off can shatter investors' faith in a company or uncover a fraud. Just so, the law takes a very hard stance against those who are either appointable or not appointable as an auditor.

This is where Section 141(3) of the Companies Act 2013 comes into the picture.

I’ve seen companies treat auditor appointments as a routine compliance item—“same CA as last year, just file the form.” But auditor independence is not a checkbox exercise.

Moreover, if the appointment itself violates the provision in Section 141, then the very legality of the audit becomes questionable despite the accuracy of the numbers.

Why Section 141 Exists in the First Place

Before delving into the intricacies of Sec 141(3) of the Companies Act 2013, it is important to know the philosophy behind this section.

An auditor’s work can be described as follows:

- Examine financial statements objectively

- Question management where needed

- Report truthfully to shareholders

If the auditor has any financial, professional, or personal connection to the business, then the auditor is not independent.

So, Section 141 of the Companies Act 2013 states that

Who is eligible to be appointed as an auditor

Who Is Disqualified, Even if Technically Qualified?

Basic Eligibility: Who Can Be an Auditor?

Let's discuss the foundation first.

Under the Companies Act, a person can qualify to be appointed as an auditor only if the person is a chartered accountant This is non-

The audit of a company can be conducted by:

- An individual Chartered Accountant, or

- A firm of Chartered Accountants (where the signing partner is a CA)

This requirement ensures professional competence—but competence alone is not enough. Independence matters even more.

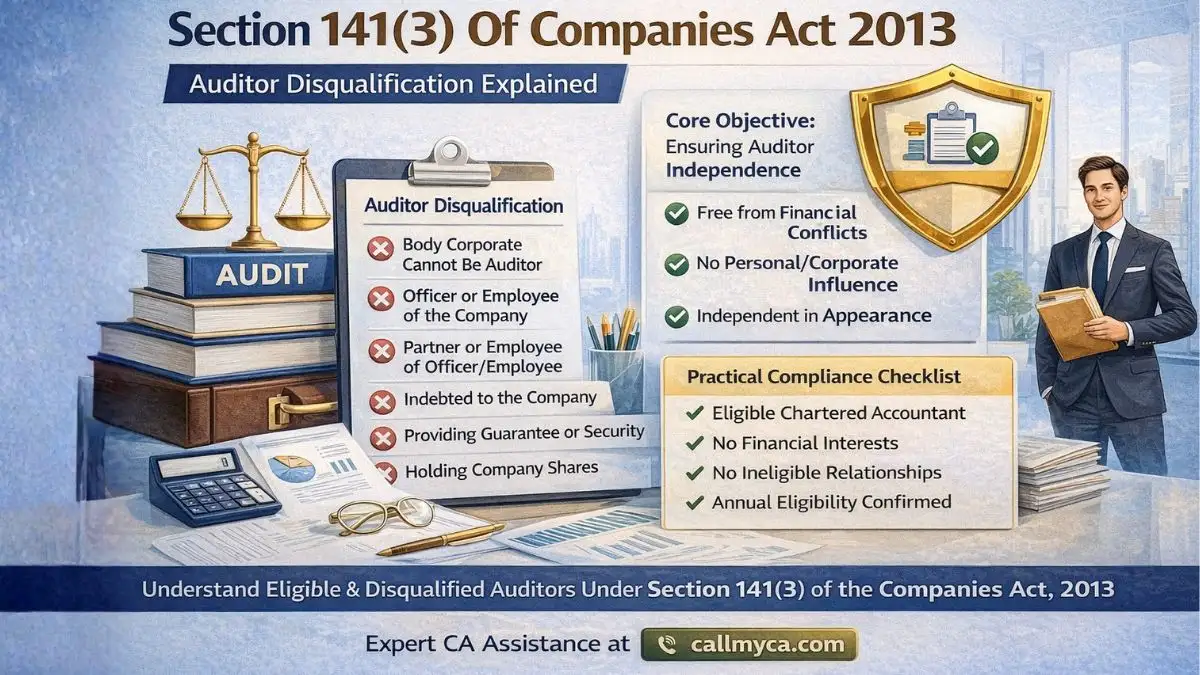

What Is Section 141(3) of the Companies Act 2013?

Section 141(3) of the Companies Act 2013 specifically lists persons or entities that are disqualified from becoming an auditor, even if they are otherwise qualified chartered accountants.

In simple words:

You may be a CA, but certain relationships with the company automatically disqualify you from auditing it.

These disqualifications are designed to eliminate conflicts of interest and protect the credibility of the audit process.

Core Objective of Section 141(3)

The heart of Section 141(3) of the Companies Act 2013 is auditor independence.

The law wants to ensure that:

- The auditor is not auditing their own work

- The auditor is not influenced by financial dependence

- The auditor is not under management control

An auditor must be independent in fact and appearance.

1. A Body Corporate Cannot Be an Auditor

Under Section 141(3) of the Companies Act 2013, a body corporate is disqualified from being appointed as an auditor.

This means:

- A company cannot be an auditor

- An LLP cannot be an auditor

Only individuals or firms of chartered accountants are permitted.

Why?

An audit is a professional responsibility, not a corporate activity driven by shareholders or boards.

2. Officer or Employee of the Company

An officer or employee of the company cannot act as its auditor.

This includes:

- Directors

- Key managerial personnel

- Payroll employees

You simply cannot audit the organization you work for.

This rule also extends to:

- Holding companies

- Subsidiary companies

- Associate companies

The idea is simple: no internal auditing disguised as a statutory audit.

3. Partner or Employee of an Officer or Employee

Even indirect relationships matter.

Under Section 141(3) of the Companies Act 2013, a person is disqualified if they are:

- A partner of an officer or employee of the company

- An employee of such officer or employee

This prevents backdoor influence over the auditor.

4. Indebtedness to the Company

One of the most practical and commonly violated clauses.

An auditor is disqualified if:

- They are indebted to the company, its holding, subsidiary, or associate

- The amount exceeds the prescribed limit

Loans, advances, or outstanding dues can destroy independence.

Why this matters:

An auditor who owes money to the company may hesitate to issue an adverse remark.

5. Providing Guarantee or Security

If the auditor has:

- Given any guarantee, or

- Provided security in connection with indebtedness of a third party to the company

They are disqualified under Section 141(3) of the Companies Act 2013.

This ensures auditors don’t have indirect financial exposure tied to the company’s fortunes.

6. Holding Securities in the Company

An auditor cannot hold:

- Shares

- Debentures

- Other securities

In the company, its holding, subsidiary, or associate.

Even a small investment can create bias—especially when audit opinions affect share value.

7. Significant Business Relationship

This is one of the most nuanced disqualifications.

An auditor is disqualified if they have:

- A business relationship with the company

- Other than professional services permitted by law

Examples of problematic relationships:

- Consultancy contracts

- Vendor arrangements

- Revenue-linked engagements

Audit fees should be the only significant financial connection.

8. Relative Relationships

If a relative of the auditor:

- Is a director or key managerial personnel

- Holds securities beyond prescribed limits

The auditor may become disqualified.

This ensures independence extends beyond the individual to their immediate financial ecosystem.

“The Auditor So Appointed Shall Fulfill the Criteria…”

A key compliance principle often ignored is this line:

The auditor so appointed shall fulfill the criteria provided in Section 141

This means:

- Eligibility is not a one-time check

- Criteria must be fulfilled throughout the tenure

If a disqualification arises later:

- The auditor must vacate the office.

- The company must appoint a new auditor

Relationship with Other Sections

To avoid confusion, let’s clarify how this fits into the broader law.

- Section 141 of Companies Act 2013 – Eligibility & disqualification of auditors

- Section 141(3) – Specific disqualifications

- Section 142 of Companies Act 2013 – Auditor remuneration

- Section 144 of Companies Act 2013—Prohibited non-audit services

Together, they create a full independence framework.

Common Practical Mistakes Companies Make

From real compliance reviews, here are recurring issues:

- Continuing the same auditor despite new conflicts

- Ignoring relative shareholding disclosures

- Overlooking group company relationships

- Treating consultancy income as “insignificant”

- Not reassessing eligibility every year

Most violations are accidental—but penalties don’t distinguish intent.

Consequences of Violating Section 141(3)

If an auditor is appointed in violation of Section 141(3) of the Companies Act 2013:

- The appointment can be declared invalid

- Audit reports may lose credibility

- Regulatory penalties may apply

- Directors may be held responsible

In severe circumstances, it can lead to red flags involving governance during inspection/due diligence.

Section 141(3) Amendment and Evolution

Various searches for section 141 (3 g of the Companies Act 2013 amendment) demonstrate the growth of interpretations.

The spirit, however, remains unchanged:

Independence over convenience.

Similarly, amendments and rule-making polish details of thresholds and disclosures, without altering the essence of the core principle.

Practical Compliance Checklist for Companies

Before making an appointment or an audit assignment, it is important to always ask:

He is an ‘Auditor’ by profession.

No direct or indirect financial interest

No prohibited business relationships

No disqualifying relative connections

Eligibility confirmed annually

This checklist can prevent years of litigation risk.

For expert guidance on auditor eligibility, compliance under Section 141(3), statutory audit appointments, and corporate governance matters under the Companies Act, 2013, connect with experienced professionals at callmyca.com for reliable, practical, and compliant solutions.